Divine Treatment Of Bad Debts In Cash Flow Statement

Where In The Cash Flow Statement Will Bad Debts Written Off Be Placed Quora International Financial Reporting Standards Committee What Is An Unaudited Profit And Loss

Bad Debts In Cash Flow Statement Llp Balance Sheet Format Excel Operating Investing Financing

Negative Cash Flow Investments In Companies Using Financial Ratios To Assess Performance Trial Balance Is Prepared On

Cash Flow Statement How A Of Flows Works Michelin Financial Statements Functional Balance Sheet

/dotdash_Final_Cash_Flow_Statement_Analyzing_Cash_Flow_From_Investing_Activities_Jul_2020-01-5297a0ec347e4dd8996f307b3d9d61ad.jpg)

Cash Flow Statement Analyzing From Investing Activities Balance Sheet Reconciliation Means The Fitness Studio Incs 2018 Income

Bad Debt Overview Example Expense Journal Entries Multi Step Financial Statement Paying Interest And Receiving Revenue Are Examples Of

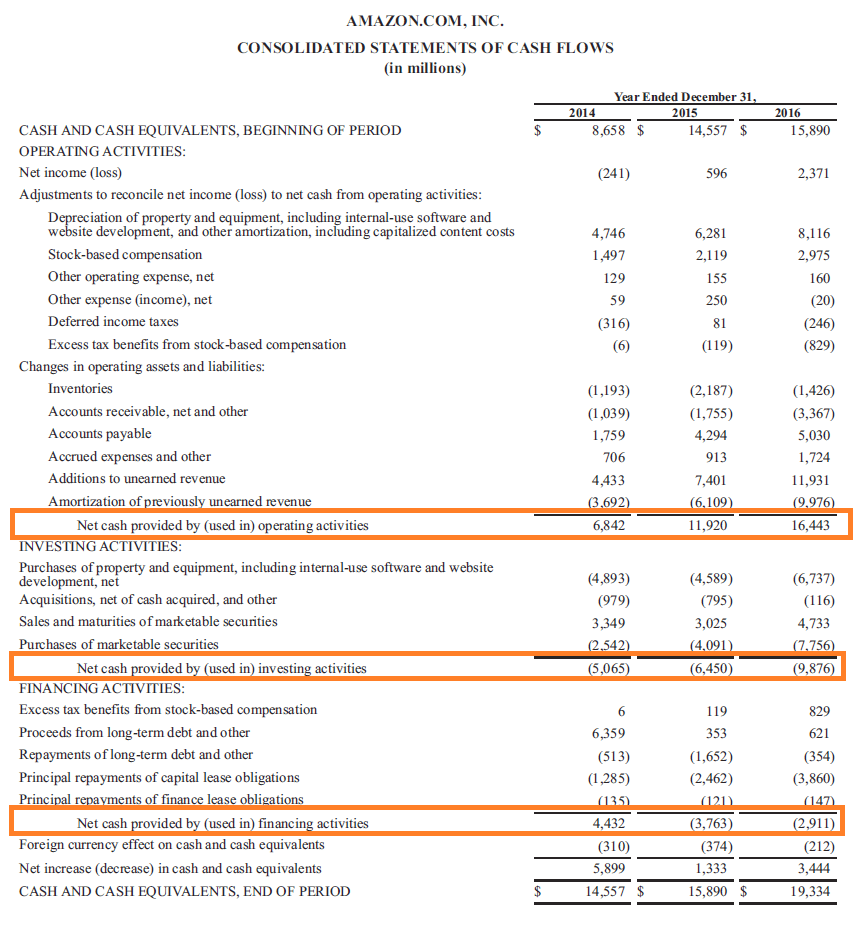

In recent years the FASB issued ASU 2016-152 and ASU 2016-183 which clarified guidance in ASC 230 on the classification of certain cash flows and removed some of.

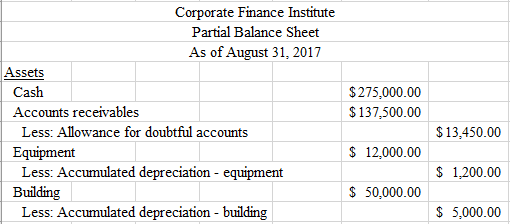

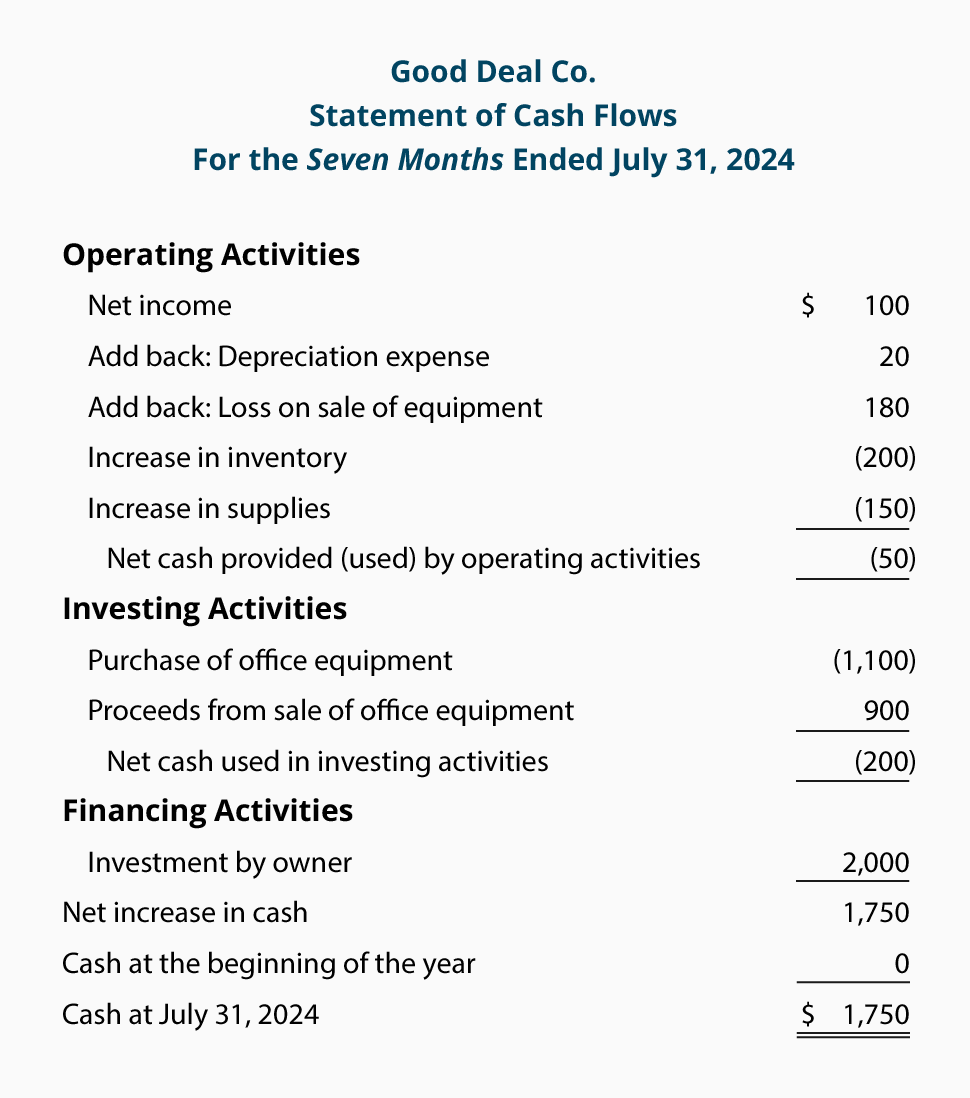

Treatment of bad debts in cash flow statement. A customer goes out of business and fails to pay its 5000 invoice. Debt is the amount which is recoverable from a person or entity. Capital and related financing.

It depends what the provision is. Reduces profit but does not impact cash flow it is a non-cash expense. Has no bad debt reserves.

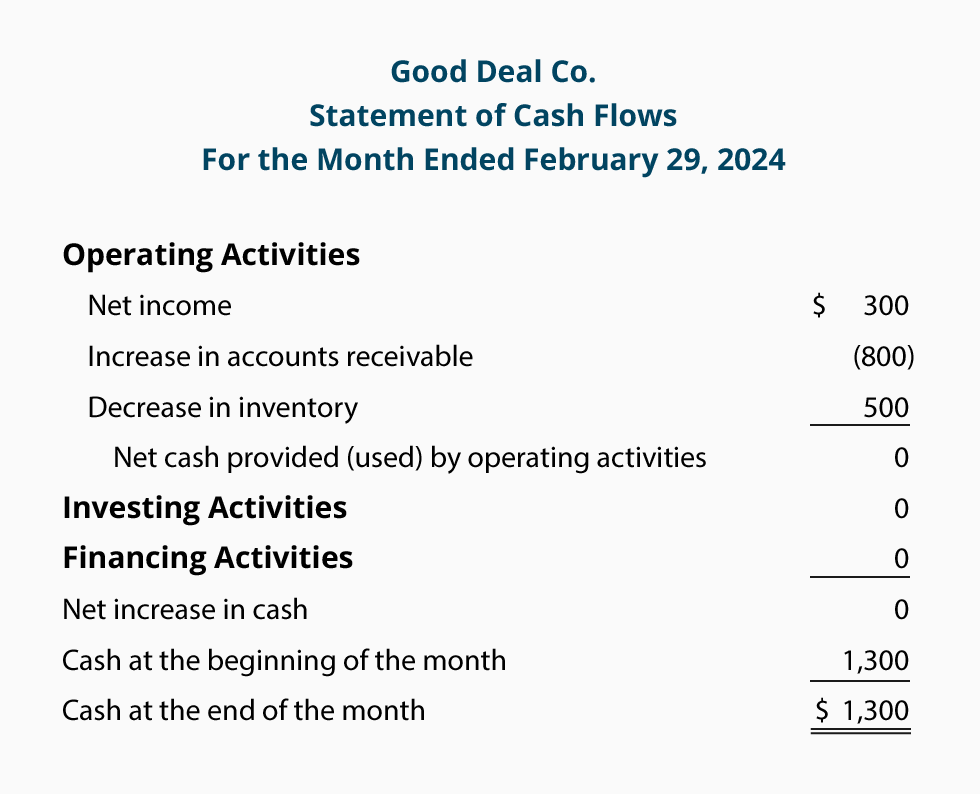

Statement of Changes in Financial Position Cash Flow Statement Bad debt expense also appears as a non-cash expense item on the Statement of changes in financial position Cash flow statement. Removal of expenses to be classified elsewhere in the cash flow statement eg. What is the treatment for bad debts written off against provision for bad debts in cash flow statement.

The cash flow statement doesnt. Elimination of non cash expenses eg. If its a provision for doubtful debts or for depreciation then no they wont appear as line items in the statement of cash flows.

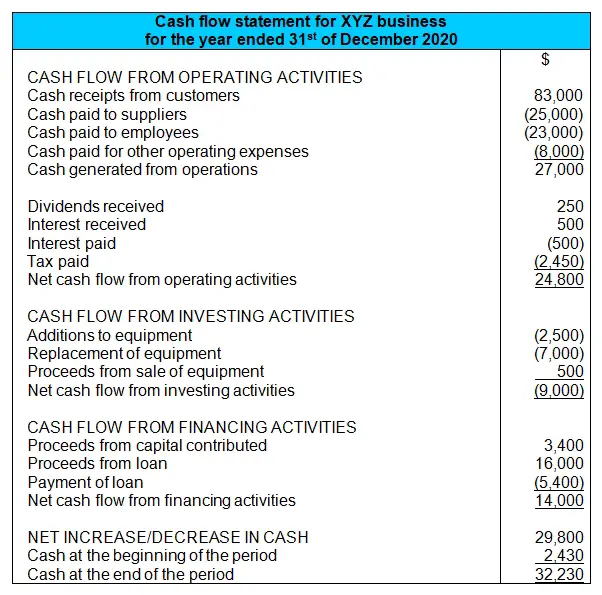

Use the following four categories of activities to classify cash transactions. Even though our net income listed at the top of the cash flow statement and taken from our income statement was 60000 we only received 42500. An Example of Bad Debt Reporting Assume a company called Newco Inc.

Depreciation amortization impairment losses bad debts written off etc. Debited in PL AC is to be added back as non cash item and the changes in the Balance of the Prov. My assumption is that the prov.

Cash Flow Statement How A Of Flows Works Fair Value Through Profit And Loss Journal Entries P & L Finance

/dotdash_Final_Cash_Flow_Statement_Analyzing_Cash_Flow_From_Financing_Activities_Sep_2020-01-bb839165006243148d0fd854ee5f477f.jpg)

Cash Flow Statement Analyzing Financing Activities Different Kinds Of Financial Statements Assets Liabilities Equity Calculator

:max_bytes(150000):strip_icc()/dotdash_Final_Cash_Flow_Statement_Analyzing_Cash_Flow_From_Financing_Activities_Sep_2020-01-bb839165006243148d0fd854ee5f477f.jpg)

Cash Flow Statement Analyzing Financing Activities Short Term Investments Balance Sheet Google Sheets

Sinking Fund A To Help You Sink Your Debt In 2021 Funds Finance Investing Accounting Profit And Loss Account Income Statement Understanding Of Financial Position

Cash Flow Statement And Depreciation Uses Of Fund Pdf Analysis Annual Report A Company

Cash Flow Statement How A Of Flows Works Intc Balance Sheet Pre Tax Income On

Disposal Of Assets Accountingcoach Formula For Operating Income Concept Fund Flow Statement

Cash Flow Statement Definition And Meaning Bookkeeping Business Learn Accounting Cigna Financial Statements Net Profit Loss In Balance Sheet