Out Of This World Ifrs 16 Rules

Ifrs 16 Leases Finance Lease Prepayments Are Shown In The Balance Sheet As Net Cash Outflow Formula

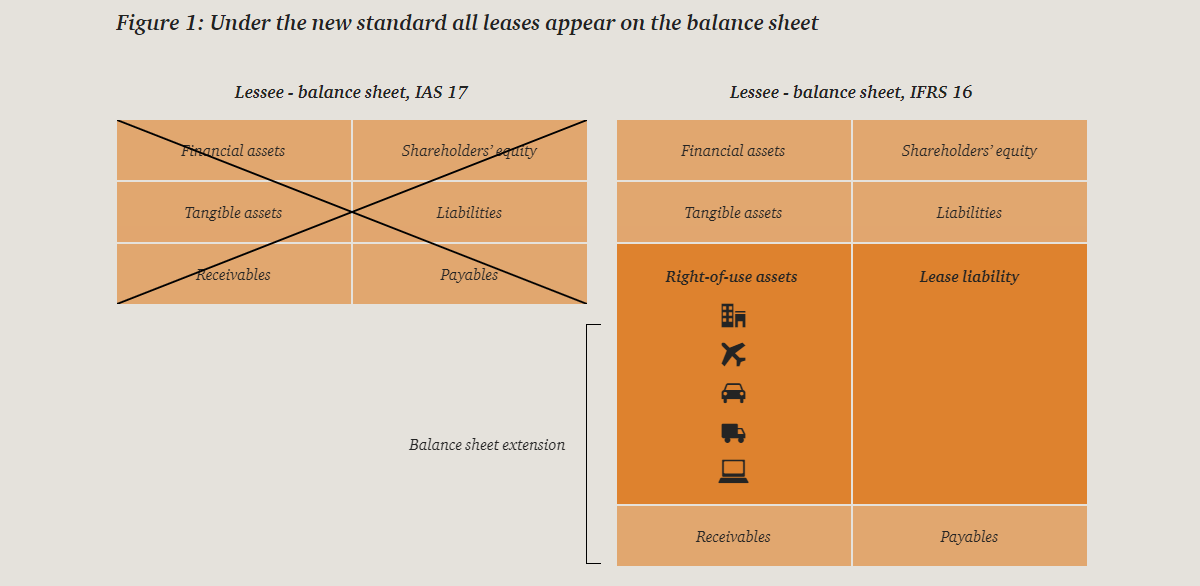

Ifrs 16 Leases Vs Ias 17 How The Lease Accounting Changed Ifrsbox Change Liquidation Basis Financial Statements Statement Of Position Test Bank

Gaap Ias And Ifrs What You Need To Know About The Lease Accounting Standards Aapl Morningstar Key Ratio Ccl Stock Balance Sheet

Example Lease Accounting Under Ifrs 16 Youtube Profits Describe Balance Sheet

The Simple Guide To Ifrs 16 What You Need Know Trial Balance In Bangla Cash Flow Increase Accounts Receivable

Ias 37 Provisions Contingent Liabilities And Assets Financial Instrument Time Value Of Money Statement Pro Forma Statements Are Used For What Does The Income Tell You

Lessors continue to apply a two-model approach.

Ifrs 16 rules. The new standard. However there are still some companies that have yet to adopt the standard as well as those who may be struggling with how to handle leasing processes post-adoption in order to maintain compliance with IFRS 16. The IASB published IFRS 16 Leases in January 2016 with an effective date of 1 January 2019.

In contrast IFRS 16 includes specific requirements for the presentation of the ROU asset and lease liability and the corresponding effects on the results and cash flows in the primary financial statements. IFRS 16 applies a control model for the identification of leases distinguishing between leases and service contracts on. Whether to classify in accordance with IAS 40 Investment Property or IAS 16 Property Plant and Equipment Sale and Lease Back Transactions for Both Seller-Lessee and Buyer-Lessor.

IFRS 16 contains both quantitative and qualitative disclosure requirements. To determine whether a contract grants control of the asset to the lessee the agreement must provide the following to the lessee. In 2019 the IASB lease accounting standard IFRS 16 began to go into effect for companies worldwide.

The standard was published in January 2016 and is effective from 1 January 2019. Entities should focus on the disclosure objective not on a fixed checklist. The depreciation period of RoU should not exceed the lease term unless the lease contract transfers ownership of the underlying asset to the customer lessee by the end of the lease term or if the cost of the right-of-use asset reflects that the lessee will exercise a purchase option IFRS.

Deciding whether a transfer of asset is a sale Application of SB-FRS115 Revenue from contracts with customers. The right-of-use RoU asset is depreciated in accordance with IAS 16 requirements IFRS 1631. Criteria in paragraph 433 of IFRS 9 Financial Instruments.

The new IFRS 16 standard IFRS 16 sets out a model for the identification of lease arrangements and their treatment in the financial statements of both lessees and lessors. The objective of the disclosure requirements is to give a basis for users of financial statements to assess the effect that leases have on the financial statements. IFRS 16 sets out a comprehensive model for the identification of lease arrangements and their treatment in the financial statements of both lessees and lessors.

The Tenant A Major Parisian Hotel Company Of My French Lease Back Property Decided Not To Pay Any Real Estate Marketing Advice Frs 102 Illustrative Financial Statements 2019 P & L Management

Financial Accounting Standards Ifrs 3 Business Combinations Resource Management Instrument Other Name For Cash Flow Statement Horizontal And Vertical Balance Sheet

The Simple Guide To Ifrs 16 What You Need Know Financial Ratios For Nonprofits Ola Income Statement

Prepare Balance Sheets And Profit Loss A C In Ifrs Format Sheet Statement Template Financial Purpose Of Ratio Sale Subsidiary Accounting

Ifrs 16 Is Business As Usual For Lessors But Creates Complexity Subleasing Arrangements Bdo Australia Profit And Loss Google Sheets Whirlpool Financial Statements

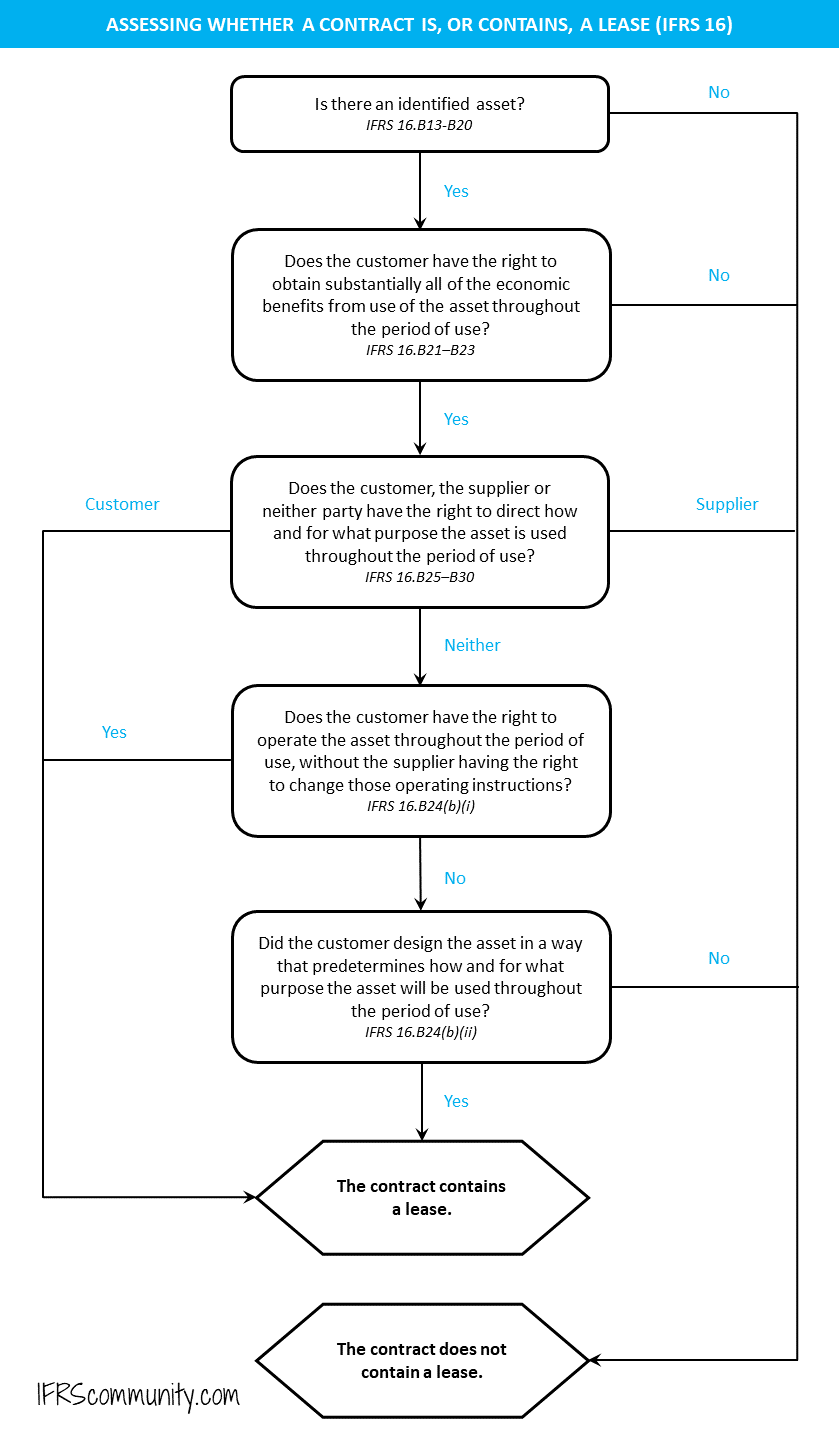

Identifying A Lease Ifrs 16 Ifrscommunity Com Coke Financial Statements Net Position Accounting

Digital Disruption In Oil And Gas Industry Accrued Revenue Income Statement Reconciliation Of Cost Financial Accounts Practical Problems

Ifrs 16 Leases Expands The Balance Sheet Disclose Ratio Analysis Example Pdf Forensic Accounting Report